Reforms : Is there a seamless story behind the seemingly disconnected and discrete set of reform measures?

It has been three years since the current regime took the reins of governance. For anyone who had expected the Govt. to unleash big-bang reforms in the early part of its term, it has been a disappointment to say the least. Much to the criticism of free market enthusiasts, Govt. has been slow on sensitive, yet significant bold reforms such as privatization of public sector banks and other non-strategic PSUs besides the revamping of archaic labour and land rules. These are bold measures, if unleashed, could have catapulted India structurally into a higher growth orbit. But to achieve a similar objective, Govt. seems to have chosen much less disruptive path (politically), yet significant in its long-term compounding effect, by systematically scripting a plot connected by seemingly discrete set of incremental reform measures. Strangely, this plot has an equal potential to propel India’s growth structurally into a higher pedigree.

To understand the plot, it is important to decipher what is behind the dots that connect the discrete measures. If there is any common thread that runs across the incremental reform measures such as DBT(targeted subsidy), RERA(Real Estate regulations), Demonetization, Bankruptcy Code, Linking of Aadhaar with PAN, Curbs on Cash transactions, Benami Act and lastly the glorious GST, it is a coherent strategy that runs seamlessly across to structurally swell the tax base and tax/GDP ratio to significantly higher levels. Early signs of such a swell is already visible on the individual tax front with personal tax kitty surging by over 20%+ annually over last 2+ years. GST would do the same magic in indirect tax numbers over time, though in the short-term, implementation hiccups would drag the numbers briefly. Deeper mining on DeMon data trail coupled with effective execution of benami act on the ground would add to the swell, both in personal tax and in corporate tax.

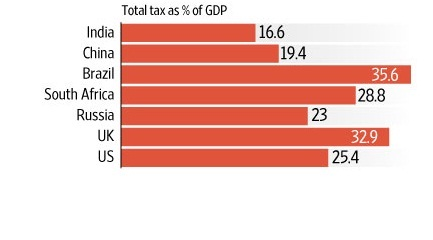

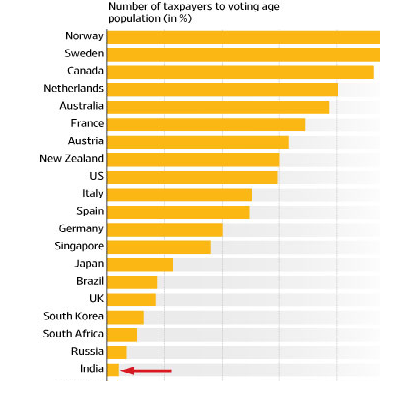

Crux of all these coherent reform measures is in compliance (tax). With India placed abysmally low on tax base as well as on tax-GDP ratio (ref below charts), these were critical measures to change the structural landscape of the economy. With expected spurt in tax kitty (widening tax net) in the coming years, it will lead to higher fiscal space over time, which will in-turn lead to structural downward shift in inflation / interest rates and thereby changing the structural capacity of economy for higher growth. As the economy shifts to more formalized (from unorganized) one on these reform measures, household savings are expected to see a dramatic shift from physical to financial assets, which will structurally push the potential growth further.

Over time, with the widening tax net along-with the changing profile of household savings (from physical to financial), India can break out of the 7%+ growth range to join the elite club of 9%+ growth. Though India has seen such a growth rate cyclically (riding on global growth as in the case of 2004-07 up-cycle), to structurally (hence more sustainable) move into that orbit will be a significant achievement for this administration. In summary, the restrained reforms of this Govt., when they play out over next few years, have the potential to have snowball effect to push economy structurally into a higher growth-orbit. No surprise that both FDI and FPI flows are in a rush. Domestic investors too are in a hurry with the trend of changing profile of household savings gathering momentum!